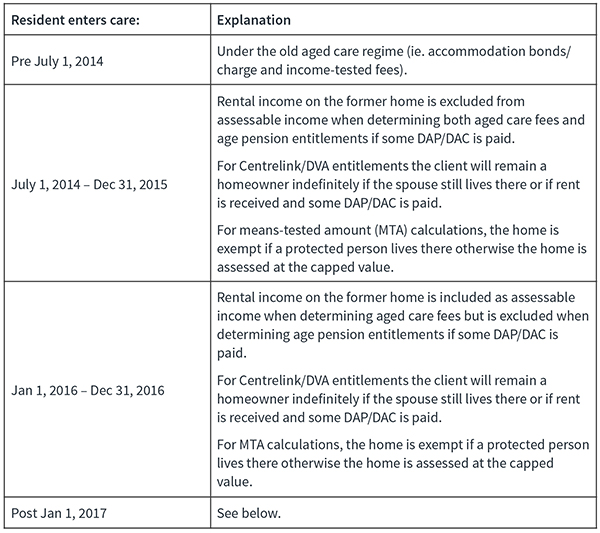

Centrelink impact of renting the former home

Residents who move into residential aged care from January 1, 2017 and rent their former home will receive less generous Centrelink/Department of Veterans’ Affairs (DVA) assessments due to changes that are now effective. The Omnibus Bill, which received Royal Assent on September 16, 2016, saw the changes first announced in the 2015 Mid-Year Economic and Fiscal Outlook passed as law. These changes became effective on January 1, 2017.

The rental income from a former home will be included as assessable income in the Centrelink/DVA income test for clients who enter residential aged care on or after January 1, 2017. The asset test exemptions will also only apply for up to two years unless a spouse is still living in the home.

Tip: The rental income on a former home is already included as assessable income in the means-test amount calculations for clients who enter residential care on or after 1 January 2016.

Background

A common strategy used in aged care has been to rent the former home and ensure that some of the accommodation payment is paid as a Daily Accommodation Payment (DAP) or Daily Accommodation Contribution (DAC). Under this strategy, the client remained a homeowner indefinitely (not just two years) when determining age/service pension entitlements, with the home remaining an exempt asset and the rental income also being exempt under the income test. The exemptions have been closed off for clients entering care from January 1, 2017.

The new rules to calculate Centrelink/DVA entitlements

If a client enters residential care from January 1, 2017, regardless of how they pay the accommodation payment the client will remain a homeowner under the assets test for a maximum of two years. At the end of this period (or when the home is sold) the person becomes a non-homeowner and the net market value of the home is included as an assessable asset. If the former home is rented, the taxable rental income is assessable income under the income test – no exemption period applies under the income test.

What it means for clients

The new rules may reduce the amount of pension otherwise payable to residents who keep their former home. This adds more pressure on cashflow and may make it more difficult for clients to afford residential care. This may increase interest in strategies such as:

- Sell the home

- Pay a part Refundable Accommodation Deposit (RAD) and request the DAP to be deducted from the RAD

- Use a reverse mortgage or aged care loan to access equity in the home.

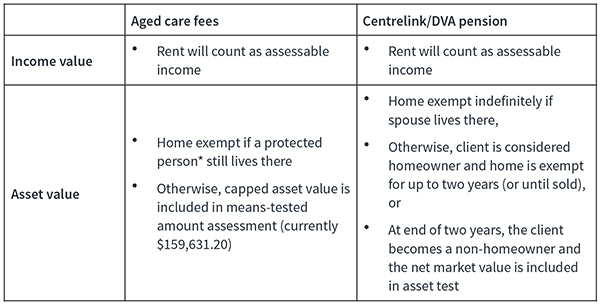

Clients in aged care will now fall into one of the following categories:

The table below shows how the former home will affect a client’s aged care fees and Centrelink/DVA pension if they move into care from January 1, 2017:

* Protected person: 1. spouse OR 2. carer (2+ years)/close relative (5+ years) and eligible for income support payment

Impact for couples

What happens if a client is a member of a couple where one partner moves into care before January 1, 2017 and the other partner moves into care after that date? Consider the example of Bert and Mary. Mary moved into care in December 2016 and Bert moves into care in February 2017. After Bert’s move they rent the former home for $26,000 per annum (after fees).

Mary’s share of rental income is exempt, but Bert’s $13,000 share is included as assessable income and added to all other assessable income generated by the couple. The total assessable income is applied to the couple income test to determine the pension payable to each. As such, Bert’s share of the rental income will impact the pension payable to both Bert and Mary.

Bert and Mary will continue to be assessed as homeowners under the assets test with the home an exempt asset for the longer of:

- Two years from Bert’s entry into aged care, or

- Mary’s death.

Bert’s means-test amount will be calculated using assessable rental income of $13,000 and a capped asset value on the home of $159,631.20. Mary’s means-test amount calculation will do the same.